In order to facilitate meetings of the board and the shareholders (including the annual general meetings of shareholders) without physical presence during the three-months emergency period triggered by the COVID-19 pandemic, the Luxembourg legislator has set up the regulation of 20 March 2020 (the “March 2020 Regulation”).

As the state of emergency finally ended on 24 June 2020, some of these measures aiming at maintaining social distance have been extended by the law of 20 June 2020 (the “June 2020 Law”).

The below mentioned rules for meetings of the board and the shareholders (the “Measures”) apply to all companies including Luxembourg investment funds of the corporate type even if the articles of association of the relevant company do not provide for such possibility and regardless of the number of participants.

In accordance with the June 2020 Law these Measures shall apply for the duration of the extension provided by article 3 of the law of 22 May 2020 (which has extended the deadlines for the approval and filing of annual accounts) (the “May 2020 Law”).

Consequently, these Measures should apply to meetings held during the extension period for the approval and filing of the annual accounts (i.e. extension period of nine months as from the end of the last financial year of a company) (the “Extension Period”).

For example, companies whose last financial year ends on 31 December 2019 may benefit from the provisions of the June 2020 Law until 30 September 2020 and will also benefit from the May 2020 Law which has extended the deadlines for the approval and filing of annual accounts. Such companies have to approve their annual accounts until 30 September 2020 and to file/publish their annual accounts and associated reports until 31 October 2020.

At the end of the Extension Period, the companies which have decided to continue to take decisions virtually or by means of written resolutions shall review their articles of association and amend them, if necessary, to implement the Measures into their articles of association (unless already provided for in such articles of association).

This unprecedented situation is raising many tax issues, especially where there are cross-border elements in the equation. For instance, it may raise concerns about a potential change in the place of effective management of a company as a result of a relocation, or inability to travel, of board members. In that respect, OECD has issued guidelines, encouraging its members to take into account the exceptional circumstances triggered by the crisis. An analysis should however be made on a case by case basis in order to determine any potential tax risk.

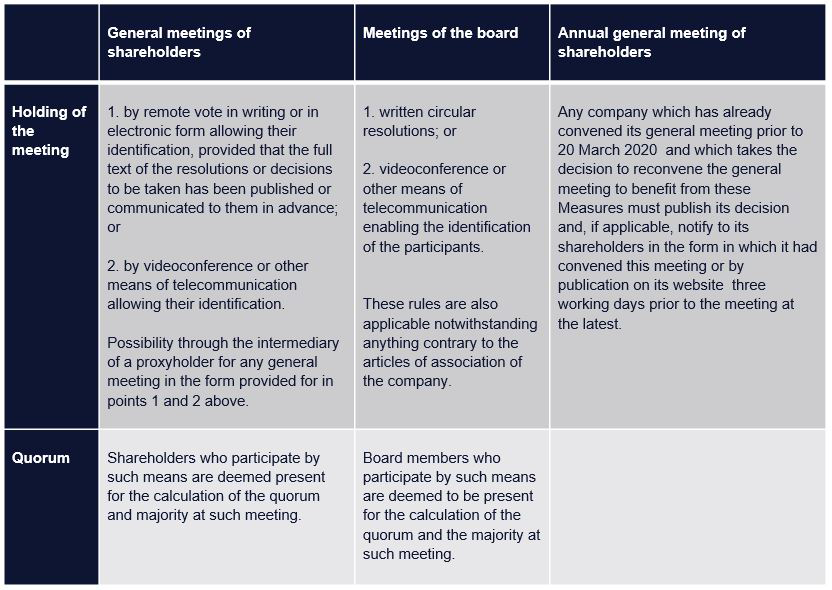

Summary of the Measures:

The companies shall review their corporate governance procedure or organise relevant identification procedure to ensure that the shareholders or board members who vote remotely or participate by video conference to the board meetings or shareholders general meetings are duly identified.

If you would like to know more about the March 2020 Regulation and its provisions taken in the COVID-19 context, we invite you to visit our page dedicated to COVID-19 on our website, or to consult the below direct links to the various laws and regulations, as well as our articles:

In order to facilitate meetings of the board and the shareholders (including the annual general meetings of shareholders) without physical presence during the three-months emergency period triggered by the COVID-19 pandemic, the Luxembourg legislator has set up the regulation of 20 March 2020 (the “March 2020 Regulation”).

As the state of emergency finally ended on 24 June 2020, some of these measures aiming at maintaining social distance have been extended by the law of 20 June 2020 (the “June 2020 Law”).

The below mentioned rules for meetings of the board and the shareholders (the “Measures”) apply to all companies including Luxembourg investment funds of the corporate type even if the articles of association of the relevant company do not provide for such possibility and regardless of the number of participants.

In accordance with the June 2020 Law these Measures shall apply for the duration of the extension provided by article 3 of the law of 22 May 2020 (which has extended the deadlines for the approval and filing of annual accounts) (the “May 2020 Law”).

Consequently, these Measures should apply to meetings held during the extension period for the approval and filing of the annual accounts (i.e. extension period of nine months as from the end of the last financial year of a company) (the “Extension Period”).

For example, companies whose last financial year ends on 31 December 2019 may benefit from the provisions of the June 2020 Law until 30 September 2020 and will also benefit from the May 2020 Law which has extended the deadlines for the approval and filing of annual accounts. Such companies have to approve their annual accounts until 30 September 2020 and to file/publish their annual accounts and associated reports until 31 October 2020.

At the end of the Extension Period, the companies which have decided to continue to take decisions virtually or by means of written resolutions shall review their articles of association and amend them, if necessary, to implement the Measures into their articles of association (unless already provided for in such articles of association).

This unprecedented situation is raising many tax issues, especially where there are cross-border elements in the equation. For instance, it may raise concerns about a potential change in the place of effective management of a company as a result of a relocation, or inability to travel, of board members. In that respect, OECD has issued guidelines, encouraging its members to take into account the exceptional circumstances triggered by the crisis. An analysis should however be made on a case by case basis in order to determine any potential tax risk.

Summary of the Measures:

The companies shall review their corporate governance procedure or organise relevant identification procedure to ensure that the shareholders or board members who vote remotely or participate by video conference to the board meetings or shareholders general meetings are duly identified.

If you would like to know more about the March 2020 Regulation and its provisions taken in the COVID-19 context, we invite you to visit our page dedicated to COVID-19 on our website, or to consult the below direct links to the various laws and regulations, as well as our articles: